Switching banks may seem like a hassle, especially if you’ve been a loyal customer of your current financial institution for a lengthy period.

However, doing so can save you a considerable amount in fees, earn you a higher interest rate on your money, and provide you with access to better products and customer service.

Here’s how to switch banks in six easy steps.

1. Know Why You’re Making the Switch

Before scouring the market for a new financial institution, it’s crucial to understand what prompted you to seek out a new bank in the first place.

Are you unhappy with the current rate of return on your savings account? Do you want a broader range of investment products to choose from? Are you dissatisfied with the lack of online banking features? Do you feel like you’re paying too much in fees relative to the level of service you receive?

By knowing the reason(s) that prompted you to consider a new financial institution, you can better identify your needs, preferences, and goals when it comes to banking.

As a result, you’ll be able to quickly narrow your options when evaluating alternative banks and ensure you select the one perfect for you.

|

OUR PICK!

|

|

LEARN MORE |

2. Evaluate Options

When choosing a bank in Canada, you have numerous options at your disposal.

The largest and most prominent financial institutions in Canada are the Big Five banks: RBC, TD, BMO, Scotiabank, and CIBC.

Exploring these brands is an excellent place to start.

While the Big Five dominate the industry and are likely to satisfy your banking needs, avoid overlooking the smaller players, some of which operate exclusively online.

These include Tangerine Bank, Laurentian Bank of Canada, HSBC Bank of Canada, Canadian Western Bank, and EQ Bank.

Jot down the name of each bank that interests you and visit the website of each one to get an idea of the types of products and services they offer.

Compare each bank based on the attributes that are important to you.

These could be interest rates, fees, rewards programs, promotional offers, investment products, or even the days and hours branches are open.

To expedite the process, there are many financial product comparison tools available online.

These sites aggregate relevant details about various banking products and conveniently present them on one page, saving you considerable time and effort.

Did You Know ?

Canadian Tire has a banking subsidiary called Canadian Tire Bank, which is classified as a Schedule 1 bank in Canada.

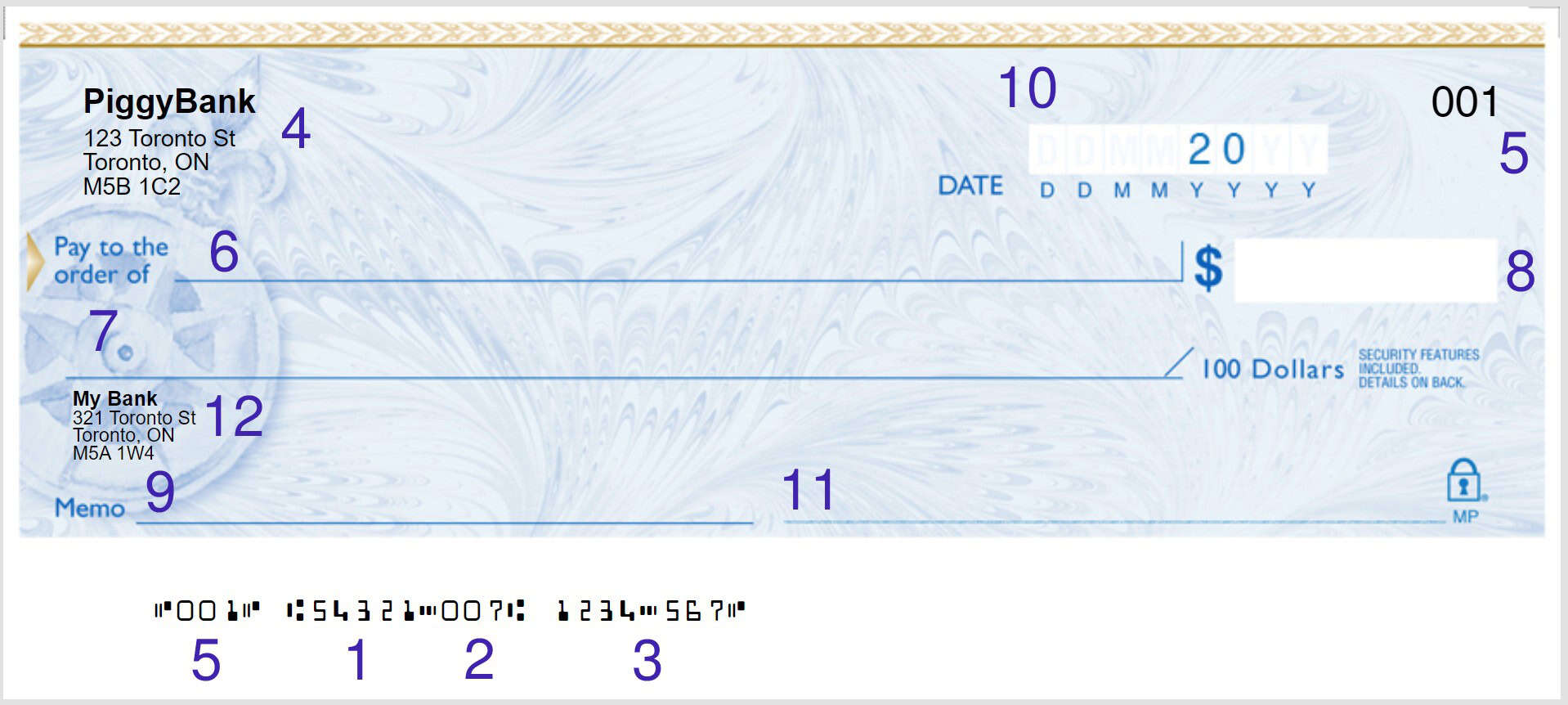

3. Open New Account

Once you’ve selected your ideal bank, it’s time to open your new account.

Your first account will likely be a chequing account since you need a place to keep your money for your day-to-day transactions.

However, you can also set up a savings account, self-directed investing account, Registered Retirement Savings Account (RRSP), and more, depending on your needs.

Some opt for a hybrid bank account as it combines features of both chequing and savings accounts.

See our types of bank accounts guide for further details.

To complete this step, you may have the option to establish your account online through the bank’s website.

If not, you’ll need to visit your local branch.

A customer service representative will guide you through setting up your account.

In general, to open an account, you’ll need to:

- Fill out a form with personal details such as your full name, address, and occupation

- Provide two pieces of valid identification

Don’t Forget!

While a social insurance number isn’t usually necessary for a chequing account, you may need to supply one if you want to open a savings account.

4. Transfer Money

Once your new account is up and running, you can transfer your money from your old bank to your new one.

There are different ways to go about it, depending on what options are available.

The easiest and most direct way is to withdraw all your money physically, take it to your new bank branch, and make a deposit.

You can also request a bank draft from your old bank, which is less conspicuous and easier to handle.

Or you can ask them to send the funds electronically.

If you opt for the latter method, it could take a few days for the money to arrive in your new account.

Unfortunately, you may also have to pay a fee.

While it’s okay to transfer the bulk of your money right away, it’s prudent to keep a reasonable amount at your old bank for at least an extra month.

You may need to settle some bill payments, loan payments, and fees linked to your old accounts that come due while you transfer banks.

5. Update Automatic Payments

Now comes the tedious step – updating all your automatic withdrawals.

Depending on how much you rely on online banking, you may have numerous pre-authorized payments linked to your old chequing account.

These include electricity, hydro, insurance, internet, and subscription like the gym.

Create a list of every bill you pay using automatic payments and methodically update the details of each account to reflect your new banking information.

This step is crucial because if a vendor attempts to pull funds from your old account, the transaction can bounce if you have already transferred all your money.

As a result, you’ll incur a non-sufficient funds fee.

Don’t forget to send your updated banking information to your employer, too, or you’ll face delays in getting your paycheque.

6. Close Old Account

Once you’ve updated your pre-authorized payments and settled all remaining financial obligations with your old bank, you can officially close your account.

Contact your bank and let them know your intention to shut down your account.

Depending on your bank’s policies, you can complete this step by phone, in person at a branch, or online.

Some banks charge a fee for closing your account, but this is typically only for those open for a few months.

You may also need to submit a formal request in writing to initiate the closure of your account.