Canadians have a myriad of choices when it comes to chequing, savings and hybrid accounts.

However, different financial services providers differ on fees, convenience, interest rates and more.

Read on for the different types of accounts available in Canada, and what to consider when making your choice.

1. Chequing Accounts

- Joint Accounts: Yes

- Currencies: CAD, USD accounts are commonly available

Think of your chequing account as your “main” bank account.

It’s likely where your employer will deposit your payments, and from where you’ll pay your bills.

Main Consideration(s) When Choosing a Chequing Account

What are the fees?

Depending on how you use it, paying a small monthly fee for unlimited e-Transfers or ATM withdrawals might be better than getting dinged with individual fees.

Consider:

- The monthly cost of the account itself

- How many free withdrawals you get per month

- How many free e-transfers you get per month

- Overdraft charges

- How much cheques cost

Institution Type

Consider the big 5 banks, smaller local banks and credit unions.

Will you have an ongoing need to physically go into a branch? Look for an institution with a strong branch network.

Are you interested in having your trading accounts and insurance policies at the same institution? A big bank like TD or RBC may be preferable then.

See our credit union vs bank comparison for further insight into whether a credit union is a suitable option.

What are the other perks?

Some banks offer sign-up bonuses of cash, points or other products when you move your chequing account over to them.

Key Insight:

Banks put a lot of effort into attracting students and youth, because many will stick with the same financial institution for life. Always be on the lookout for great offers!

2. Savings Accounts

- Registered Accounts: Yes. TFSA, RRSP, RESP, etc.

- Joint Accounts: Yes

- Currencies: CAD, USD accounts are commonly available

- Interest: 0.01% to 1.55%

It’s a good idea to have some cash in a savings account as an emergency fund, in addition to your chequing balance.

You can also open registered accounts, like a Registered Retirement Savings Account, to start socking money away for your golden years.

A savings account can also help to visually separate your “spending” money from cash you want to hold onto for a while.

Many banks also let you set up recurring auto-transfers between your chequing and savings accounts, so you can watch your savings grow without thinking about it.

This is a great way to build up an emergency fund.

Main Consideration(s) When Choosing a Savings Account

What’s the interest rate?

Because of inflation, if your money doesn’t earn interest, it actually loses value over time.

That’s why you want to maximize the interest rate your money earns, just for sitting there.

The savings accounts of major banks can be convenient if you already have a chequing account with them, but the interest can be as low as 0.1%.

An independent online option like Wyth Financial takes a few minutes to set up, but offers 1.55% interest.

If you keep $10,000 in there for a year, that’s an extra $154 in your pocket.

How often will you need to access the money?

A rainy day fund or emergency fund should be kept in a savings account that you can access anytime.

But if you’re saving for retirement, you might want to think about investing that money instead.

Buying ETFs, or putting your money in a robo-advisor, will get you more money than any savings account in the long term.

3. Hybrid Accounts

Hybrid bank accounts market themselves as bank-like services, complete with a prepaid credit card for spending.

They’re usually promoted toward younger consumers who want a free, no-frills account that lets them spend and save easily.

But if you read the fine print, they often lack some of the conveniences of normal chequing and savings accounts — like bill payments or direct deposits.

Pros:

- No fees

- Perks like cash back, points, and store discounts

- Use a credit card with no approval process

- Card accepted anywhere that accepts Visa or Mastercard

- Won’t hurt your credit score

- Sleek apps

- Canada Deposit Insurance Corporation (CIDC) protection

Cons:

- No or low interest

- Doesn’t help build credit

- Might not be able to pay bills with it

- Potentially no direct deposits

- Other free credit cards have better perks

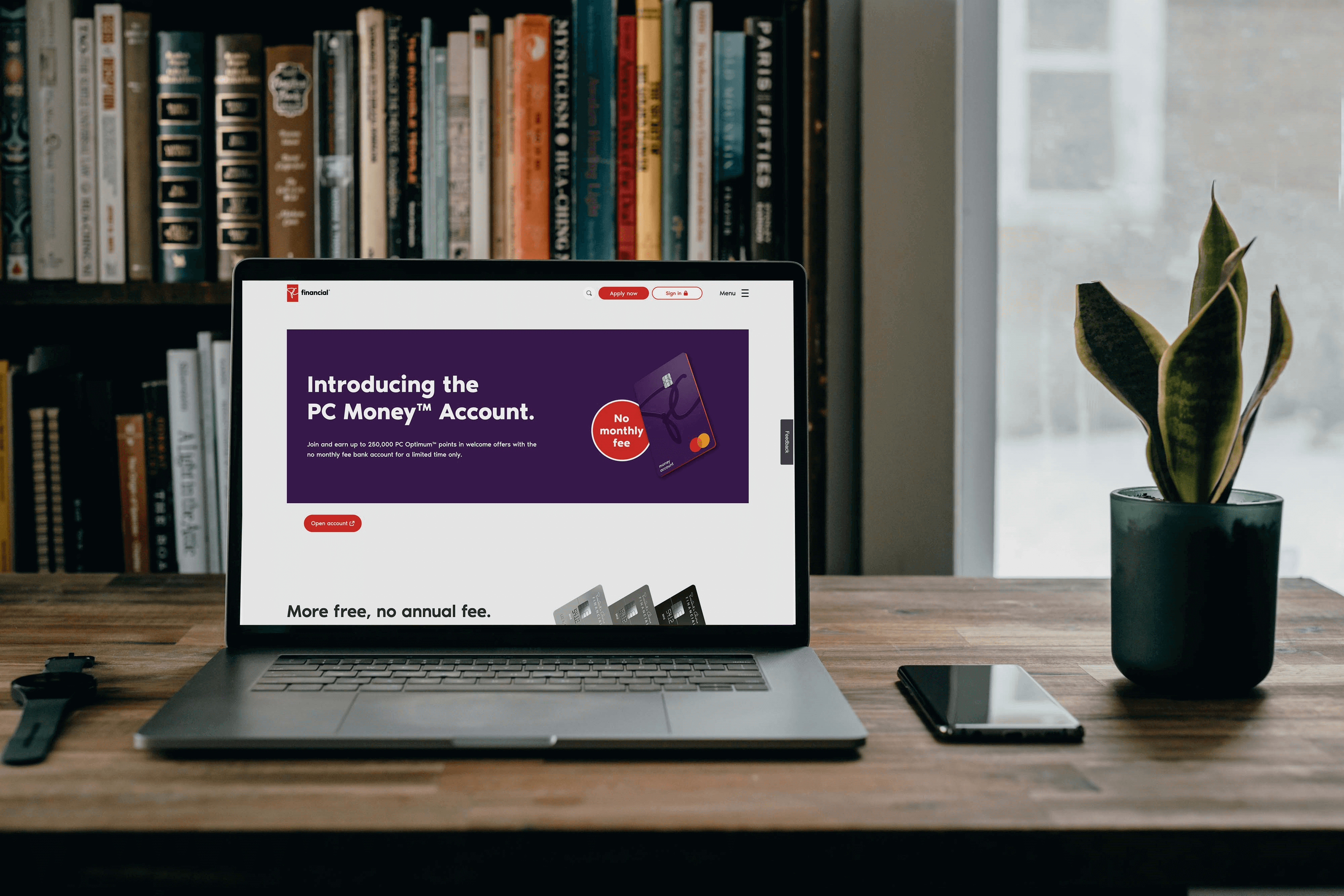

PC Money could be a good no-fee option if you use PC Optimum points often.

You can get up to 250,000 points for spending money at Presidents’ Choice stores, and referring a few friends.

That’s $250, which is a solid shopping trip or two.

And you get 10 Optimum points for every dollar you spend, anywhere, with PC Money’s prepaid Mastercard.

That’s equal to 1% cash back, but you can only redeem it at PC stores.

You also get 1,000 Optimum points per $50+ bill payment, up to 5 per month.

PC Money offers direct deposits and unlimited free e-transfers per month.

You can take out cash for free at PC Financial ATMs.

Your money doesn’t earn interest in a PC Money account.

Koho is a fee-free hybrid account with 0.5% cash back on all purchases.

You get a prepaid Visa card that debits your account.

Koho offers 1.2% interest rate if you set up direct deposits. You also get unlimited free e-transfers.

Wealthsimple Cash is another no-fee option.

If you’re already using Wealthsimple’s investment products, it’s easy to create an account.

You get a prepaid Visa card with no annual fees and 1% cash back on all purchases.

Its big selling point is that it’s something like a Canadian Venmo that allows people to send and receive money to each other’s “$igns” and split bills.

It’s easier than e-transfers and you get an unlimited number of free transfers, up to $5,000 daily and $20,000 monthly.

It doesn’t support bill payments or direct deposit, but Wealthsimple promises both are coming.

Its interest rate is zero.