As an employee, if you need to deduct employment expenses from your income when filing your tax return, your employer must complete the T2200 on your behalf.

It is an important form that should be kept safe if you are claiming employment expense deductions.

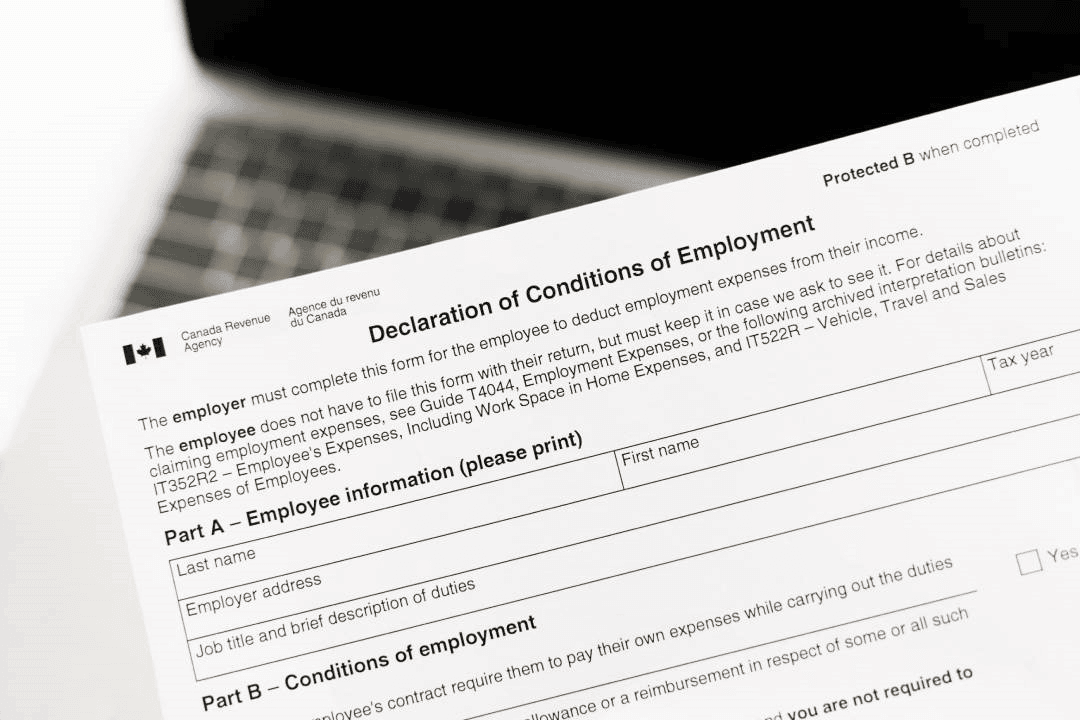

The T2200 is a form that declares the conditions of employment of an employee for work expenses incurred by the employee.

While you do not need to submit the form with your return, it should be kept safe just in case you are audited by the Canada Revenue Agency (CRA).

The form consists of two parts that must be completed by your employer.

Part A shows the employee’s information such as first name, last name, job title and description, employer address, and tax year.

Part B shows more details on the conditions of employment and requires information on the types of expenses that are incurred by the employee as a requirement for their job.

Expenses incurred could relate to travel, rent, transportation, work tools, supplies and more.

There is also an employer declaration section to affirm that the employer has provided true and accurate information.

If the CRA requests to see your T2200 form, the final section requires you to provide your name, social insurance number (SIN), and home address.

More employees are working from home fully or partly now and are looking to claim employment expenses on their tax returns.

What Expenses can I Deduct with the T2200?

Some of the eligible expenses that can be claimed through the T2200 form include:

Home expenses:

If for a period, you worked more than 50 percent of the time from your home, you may be able to claim expenses related to your workspace, eligible utilities, office supplies, cell phone, and long-distance calls, amongst other expenses.

For your workspace-in-the-home expenses to be eligible, the workspace should only be used for work-related needs required to earn income from your employment.

You are not allowed to claim mortgage interest, capital cost allowance, principal mortgage payments, capital expenses, etc.

See a detailed list of eligible and non-eligible home expenses here.

As an employee earning commission income, you can also claim expenses for property taxes, home insurance, lease of a cell phone, computer, laptop, tablet, fax machine and more.

Accounting and legal fees:

If you paid for accounting services to file your income tax, this can be claimed through the T2200 form.

Also, if you incurred legal expenses to support your right to receive your salary, or other monies not directly paid by your employer, but reported in your employment income, you can claim these expenses through the T2200 form.

Motor vehicle expenses:

Some motor vehicle costs are allowable to claim.

This includes capital cost allowance.

As a salaried employee, to claim vehicle expenses, you need to be normally required to work somewhere other than your employer’s place of business or in different places.

You also need to be required by your employer to pay for your motor vehicle expenses as shown in your contract of employment and you should not have received a non-taxable allowance for your expenses.

You can find more information on motor vehicle expenses on the CRA website.

Food, beverages, and entertainment:

As an employee earning commission income, if you want to claim food and beverages expenses, your employer must require that you are away for not less than 12 consecutive hours and you must be out of the municipality of your usual place of employer-work location.

Generally, the amount you can claim is the lesser of 50 percent of the amount you paid or the amount that is considered reasonable under specific circumstances.

For entertainment expenses, partial amounts spent on entertaining clients can be deducted.

Like the food and beverage expenses, a 50 percent limit also applies to entertainment expenses.

Salaried employees cannot claim entertainment expenses but may claim traveling expenses for food, beverage, and transportation expenses (not related to motor vehicle expenses).

Similar to vehicle expense claims, you need to be normally required to work somewhere other than your employer’s place of business or in different places.

You also need to be required to pay for your travel expenses as shown in your contract of employment, and you should not have received a non-taxable allowance for your travel expenses.

Generally, expenses that have been reimbursed by an employer cannot be deducted when reporting your income tax and benefit returns.

Lodging:

Generally, if you are required to travel for work and you are responsible for your lodging expenses, you can claim work-related lodging expenses.

Parking costs:

Some parking costs are eligible for deductions.

However, costs for parking at an employer’s office or traffic penalty fees cannot be deducted.

Advertising and promotion:

Only employees earning commission income can claim deductible expenses for advertising and promotion such as amounts paid for business cards, promotional gifts, and other forms of advertisements.

Other deductible expenses

include work supplies, eligible work tools or special clothing, office rent, medical underwriting fees, salaries for assistants, bonding premiums, licenses, and training expenses.

In claiming your deductible expenses, you will need to fill in Form T777, Statement of Employment Expense to calculate the total employment expenses amount.

This amount will then be entered on line 22900 of your tax return for the year.

While you do not need to submit the T2200 form, you need to include Form T777 with your tax return.

How Do I Get a T2200 From My Employer?

Most employers automatically issue T2200 forms to qualifying employees.

If you have employment expenses that are eligible for deduction and you have not received a T2200 form from your employer, it is recommended to contact the human resources department.