A margin account is a type of brokerage account that allows you to borrow from your broker to purchase additional securities, with the amount you can borrow being based on current value of your investing portfolio.

Most Canadians are familiar with a home equity line of credit (HELOC) that allows homeowners to essentially use the built-up equity in their real estate assets to finance other purchases.

Similar to using a line of credit against your real estate equity, investors can tap the collateral held in their brokerage account (stocks, bonds, mutual funds) and borrow against those financial assets.

The loan provided is called the margin amount and is subject to guidelines provided by the broker to identify marginable securities against which they’re willing to lend.

For those looking for leverage in trading, margin accounts are the go to product.

How Does a Margin Account Work?

Margin accounts provide investors with the ability to borrow money from their broker to enhance their buying power.

The accounts holdings (cash and securities) are considered collateral against which the broker lends additional funds, which represent the increase in buying power of the account.

Upon utilization of buying power, the investor will pay interest on the borrowed amount until the position is squared off.

Interest rates vary from broker to broker but are significantly cheaper than unsecured personal loans/credit cards.

Furthermore, this loan depends on the value of the portfolio and significant price moves may increase/decrease maintenance margin limits associated with the account.

Once securities are acquired using margin, the borrower has to satisfy margin requirements ensuring that there is sufficient liquidity to pay back the margin loan and protect the broker’s principal.

Generally, the buying power is defined using the initial margin and subsequently, one has to ensure there is sufficient liquidity to meet maintenance margin requirements.

It is common practice for margin accounts to have 30-50% margin for specified securities.

Most well-known companies would fall in this category.

For simplicity purposes, let’s assume you have 50% margin provided by your broker.

In a scenario where you wanted to buy Company X shares worth $10,000, you can buy these shares with only $5,000 of your own cash or 50% of the total value.

In the table below, as Company X shares increase in value, there is a subsequent increase in the buying power and a decrease as the price falls.

If Company X drops 50%, the investor will face a margin call as the value of the Company X position is now underwater and the broker will liquidate his/her position to recover the initial margin amount of $5,000.

At this stage, the buying power will reflect the decrease in account value and will be capped at $10,000.

| Company X Price: $166.67 | Buying Power (50% Initial Margin) | Company X position (60 shares) |

Maintenance Margin (45% Margin) |

Cash | Total Value |

|---|---|---|---|---|---|

| Account Value | $20,000 | – | – | $10,000 | $10,000 |

| Company X up 25% ($208.33) | $22,500 | $12,500 | $5,500 | $5,000 | $12,500 |

| Company X down 50% ($83.33) | $10,000 | $5,000 | $5,500 | $5,000 | $5,000 |

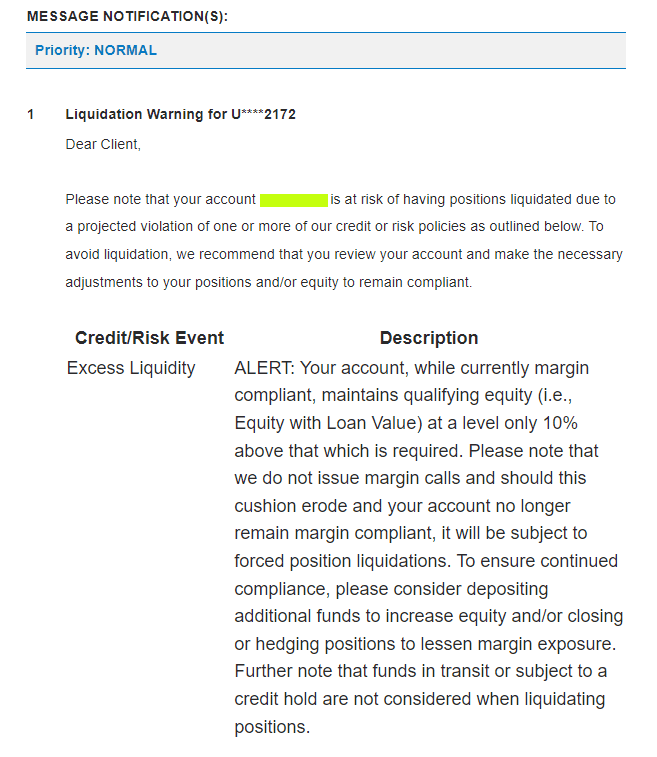

What is a Margin Call?

The perils of borrowing money to make investments are that when positions go against you, the broker will make demands to furnish additional collateral if there is a material decrease in the underlying position, thereby falling below the maintenance margin requirements.

Oftentimes, this is an auto-generated notification from the broker and not an actual phone call unless it is a significant account for the brokerage.

To remedy this situation, an investor can post more collateral (cash or marginable securities) or unwind/flatten the position.

Usually, investors using margin accounts should exhibit discretion while using leverage and focus on avoiding portfolio concentration to avert margin calls.

Margin Account vs Cash Account

The main difference between a margin account and a cash account is that a margin account allows you to borrow against your portfolio value to increase your buying power.

Most investors are familiar with having a cash account, which is extremely simple to understand and is exactly what it sounds like.

Investors open an account with a broker and fund the account using a bank deposit/wire transfer.

Once the funds are received by the broker, one can buy securities using up to the amount of cash deposited.

A Margin Account allows borrowing against a portfolio to enhance the buying power of a brokerage account.

While opening a margin account, the broker has to gather information regarding a client’s financial situation and provide reasonable disclaimers before approving the use of a margin account.

These accounts are a great tool to boost returns using leverage in comparison to a cash account, but are also open to more downside if the position goes against the investor.

Cash accounts are a great starting point for investing, but will not allow the investor to short stocks and take advantage of downward price momentum in a particular security/sector.

Margin accounts are important must-haves to enable short selling and the creation of market-neutral portfolios to deploy long/short strategies.

Margin accounts should be used by experienced investors that understand the impacts of employing borrowed capital and are capable of diversified portfolio construction to sidestep concentration risk, thereby minimizing the impacts of drawdowns while using leverage.

Having said that, it is important to highlight the risks of losses exceeding the initial deposit that exist in the case of margin accounts and how losses are capped to the initial deposit in the case of cash accounts.

| Cash Account | Margin Account | |

|---|---|---|

| Buying Power | Buying power is capped to the amount of funds deposited in the account. | Buying power is greater than the funds deposited with the broker (30-50% is industry standard of margin requirement). |

| Interest Charges | Since no borrowed funds are used, there are no interest charges levied by the broker. | Interest is payable on the amount of margin utilized during a specified period of time. |

| Leverage | No leverage available. | Leverage can be utilized to amplify returns. |

| Shorting Capabilities | Cash accounts are unable to short securities. | Margin accounts are required to execute short strategies. |

| Potential Losses | Maximum losses capped to the amount deposited in the account. | Losses can exceed initial deposit in margin accounts. |

Pros of Using a Margin Account

Outsized Returns

A margin account allows investors to build a larger portfolio from their limited investment.

Investors are able to earn a significantly greater return by employing leverage and if they are correct in terms of security selection, as well as market direction, they will position themselves to earn an outsized return in comparison to using a regular cash account for investing.

Derivatives Trades

Margin accounts facilitate executing derivatives trades.

While margin may not be needed to buy call/put options, it becomes essential to write options or trade futures.

Futures are important instruments to have access to as they provide exposure to a wide range of asset classes (equity indices, commodities , bonds, currencies and even crypto assets) which trade nearly 24 x 7 with a reasonable amount of liquidity in their respective markets.

Shorting Capability

Selling securities prior to owning the underlying is referred to as short selling.

Margin accounts are critical to entering into short trades and part of the operational mechanics of architecting such trades.

Shorting securities can be pivotal to portfolio construction and allow the creation of market neutral strategies that employ a long/short approach.

Cons of Using a Margin Account

Potential Drawdowns

As investors take a larger position vs using a cash account, they open themselves up to potentially larger drawdowns if these positions go against their thesis and will lead to larger drawdowns.

Additionally, losses can exceed their total deposit when using a margin account.

While using a cash account, losses are capped to the amount deposited and rarely exceed the total investment amount.

Interest Charges

Margin accounts provide leverage by borrowing funds and interest is paid on these borrowed funds which eat into the profitability of these trades.

Depending on how much spread investors are able to capture between their buy and sell, they can be caught overtrading and paying more fees to the broker without meaningfully increasing their returns.

Did You Know?

You can buy options without having a margin account. However, to write options (selling before buying), you need to have access to a margin account.

Should I Use a Margin Account?

Investors that have had exposure to different investment strategies and want to enhance their returns can benefit from using a margin account.

However, usage of a margin account depends on the goals and objectives of the individual investor, as well as their particular investing style.

Any short-selling investing method needs access to a margin account.