Short selling is a method that enables market participants to sell securities without owning the underlying security.

Such practices allow investors and speculators to capture downward price momentum in a given security by making bets that the price will decrease.

Any well-functioning market seeks to facilitate price discovery, match demand with supply and aims to lower transaction costs while making it easier to transact.

Short selling, while frowned upon by parts of the securities market, is a necessary force in the marketplace to provide liquidity, rein in unbounded speculation and aid the market in identifying appropriate price clearing levels.

Short selling is the mechanism that allows market participants to benefit from a fall in the price of a security and establish bearish bets on a particular company (or group of companies in the case of an ETF).

Institutional short-sellers seek to conduct in-depth fundamental analysis to uncover discrepancies in business reporting provided by listed companies in their underlying business metrics to spot over-valued companies.

These investors will then place sell orders with their broker who in turn will locate supply of these securities and will sell them on the open market by holding adequate margin against those sales.

Once the price goes down, the investor will buy the stock at the lower price and pocket the difference less any fees incurred during the process.

How Does Short Selling Work?

Short sales are conducted every day in the market and are a common marketplace fixture at this point.

When a short trade is initiated, the equities trading desk will seek to locate borrows of that security from custodians or other dealers to execute the short sale.

Once these borrows are located, sell orders are executed and the security is termed to be “on loan” on an open/term basis.

Like anything else, upon borrowing these securities, the client furnishes collateral and pays a fee to borrow these shares from the existing supply of inventory of that security.

Collateral

There are two types of collateral that can be given when lending or borrowing stock.

The first type of collateral is non-cash.

This is usually government debt, but may also include other types of bonds or equities.

The second type of collateral that is used is cash.

Non-cash collateral is more common in Canada and international markets while cash collateral is prominent in the United States.

Fees

There are several factors that contribute to the fee charged for a stock.

The market value of the order, counterparty borrowed from or lent to, and expected duration of the loan all play a factor in the fee, but the most important factor is the availability of the security.

Equities in which there is more supply available than is demanded in the market are known as general collateral, “GC”, easy, liquid or cold.

These tend to go at relatively low fees.

Stocks where the supply is limited, are known as specials, tight stock, hard to borrow or hot names.

These trade at higher rates than easy names.

Names can be special if there is increased demand in them due to a deal (merger and acquisitions, bought deal) or if there is just not a lot of supply to begin with (a lot of small-cap names).

At this point, any dividends/payments made by the company must be repaid to the original owners of the underlying securities.

Supply of Inventory

For short selling to work, there needs to be a pool of lendable securities.

There are two main groups of institutions that engage in lending securities: (i) Custodians, and (ii) Dealers.

Custodians hold assets for their clients which are largely pension funds and mutual funds.

The custodians are permitted to lend these assets and split the revenue with the fund whose assets they are lending.

The largest custodians in Canada are Royal Trust, State Street and CIBC Mellon.

In some instances, pension funds are large enough to have their own lending program.

The biggest example of this in Canada is Caisse de dépôt et placement du Québec (known as CDPQ for short).

The other major source of inventory are brokers/dealers.

Broker-dealers usually both borrow and lend stocks.

The stock that is received from broker dealers is either borrowed from a custodian or is the firm’s own internal position.

Working with security lenders poses a unique problem as the inventory of lenders does not remain constant.

The owner of the asset may choose to sell the securities that are on loan.

When this occurs, the lender will issue a recall notice to the borrower giving them three days to return the stock.

The borrower must then either borrow them elsewhere or cover the short position in order to obtain the stock.

If a borrower cannot produce the stock within a reasonable amount of time, the lender may purchase the securities in the market and pass the cost on to the borrower.

This is known as a “buy-in” in short selling and can initiate short squeezes.

In a nutshell, short selling revolves around borrowing and lending securities for a fee against collateral to establish exposure to downward price momentum in a particular security.

Four Steps to Shorting a Stock

1. Identify Security to Short

The first step to any short sale is to identify the company to short.

This can be a result of fundamental analysis, geopolitical factors or event-driven strategies.

2. Locate Shares to Short

Most investors will not run into any major issues while looking to execute short orders unless they are dealing with hard to borrow stocks that have reduced or limited availability.

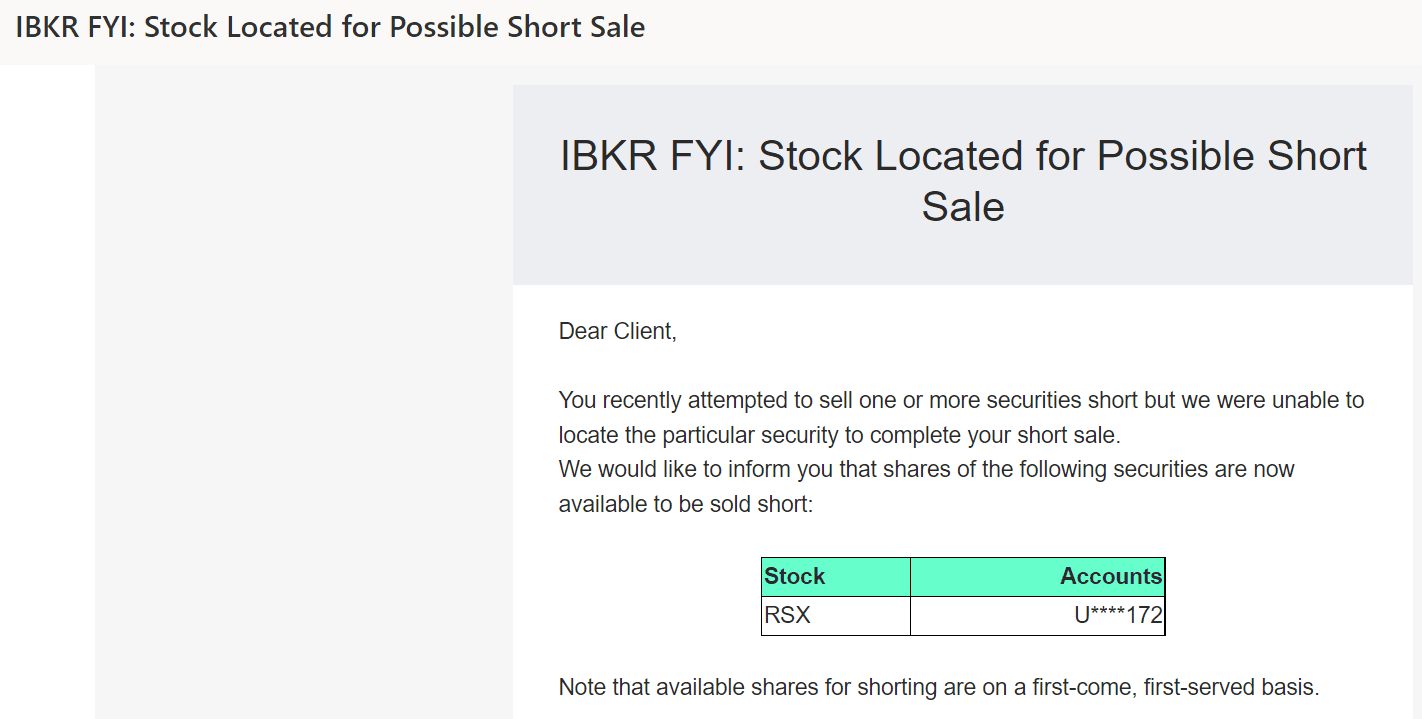

For example, investors couldn’t short the RSX ETF that tracks Russian Companies but at the same time, investors will find no difficulty in shorting a security like Apple (AAPL) which is widely held and easy to locate.

3. Execute the Short Sale

This is a straightforward step where you enter the quantity and price to sell into the open market.

At this point, your buying power in your broker account will be reduced and your positions should show a negative number of shares along with the price you received while shorting them.

4. Close the Trade

Once the trade runs its course, the investor can close the short by buying the shares shorted at a lower price than they had been borrowed for (ideally), and returning them to the lender, while keeping the profit spread.

Advantages of Short Selling

Capture Downside Momentum

The main benefit of being able to short sell is to take advantage of falling prices of a particular security.

Short selling capabilities can be extremely profitable in bearish markets as long-only funds have limited opportunities to participate in such volatility and leave money on the table.

Market Neutral Strategies

Long-short investing seeks to achieve market-neutral returns as the short side would try to hedge any downside of the long portion of the trade.

Market participants can express views on a certain sector of the economy to perform or underperform relative to each other.

Short selling can be a big part of executing such a thesis while avoiding significant market risk.

Hedging Event Risk

At times when there is significant uncertainty in the marketplace, investors can attempt to de-risk their market exposure by short selling and paring down risk appetite.

Disadvantages of Short Selling

Manufactured Payments

Beneficial owners (long-term holders) need to be compensated for any dividends and special payments that the borrowed underlying security pays to the shareholders.

As a result, short sellers have to “manufacture payments” to match these company distributions and such costs discourage short sellers from certain sectors like financial services that pay steady dividends.

Uptick Rule

The Securities and Exchange Commission (SEC) mandates short sales to be executed when the price trades higher from the last traded price.

As a result, in a vicious price move, market participants will find it difficult to short and have to wait for the uptick to enter new short positions.

This might be more relevant to day traders, but futures don’t have any such restrictions and can short at existing bid levels or lower.

Locating Securities and Borrowing Fees

Short selling profitability is dependent on how much the security falls and the borrow fee associated with shorting the stock.

However, at certain times, stocks that are falling the most (usually microcap names) are notoriously hard to locate or have exorbitant borrow fees that makes shorting hard or unprofitable.

Did You Know?

Overstock’s CEO paid a dividend in crypto to thwart bear raids on his company in Fall 2019 to short squeeze institutional sellers as they would then find it incredibly hard to borrow and manufacture dividend payments in crypto.

Why Short a Stock?

The desire to short sell a particular security can be manyfold.

Common reasons include:

- Capturing downside momentum in falling companies and sectors

- Hedging market risk

- Executing long/short portfolios and other event-driven strategies

Considerations When Short Selling

Short selling is usually conducted by active market participants that want to participate in the downward price change in a given sector or security.

However, it serves well to be cognizant of the inherent risks in short selling.

Unlimited Losses

Unlike going long a stock, which has unlimited return possibility, short selling has the possibility to have unlimited losses, and gains are capped to the sale price of the security if it goes to $0.

Bill Ackman led an activist short campaign against Herbalife in 2012 but had to throw in the towel as Herbalife zoomed higher causing his investment thesis to lose as much as a billion dollars on the trade.

Cost of Borrowing

Depending on the difficulty of obtaining the security, borrowing fees can be a massive driver on the cost of execution of short sales.

Anti-capitalistic Perception

Short selling or betting on companies to fail can be deemed to be against the free-market capitalist spirit infused into developed economies.

Public perception matters for large institutional investors operating in the public domain.