Well-diversified portfolios often allocate capital into commodities to hedge their portfolios’ inflation risks.

The most commonly traded commodities can be categorized into the following buckets: Energy (Oil, Natural Gas, Power), Metals (Steel, Nickel, Gold) and Agriculture (Wheat, Soy, Corn).

Active participants may lean in much more than the normal buy and hold investor and have outsized exposure to commodities during inflationary environments through leveraged exposure via commodity futures.

There are several paths to get exposure to commodities for investors:

1. Owning Physical Commodities

Physical commodities are probably the most direct way to grab a piece of price appreciation in a particular commodity, but they involve storage of the said commodity as well as ensuring there is a marketplace or exchange to facilitate the trade when trying to liquidate the physical commodity.

Owning and storing physical commodities is easy to accomplish for high-value commodities such as Gold, Platinum and Silver for retail investors that want to hedge their portfolios against uncertainty.

However, this strategy has limited applications for large investors that want to own a variety of commodities due to the constraints around logistics.

2. Buying Physical ETFs

Physical ETFs are great tools to get exposure to commodities with limited operational involvement in storing and maintaining physical stock of the commodity.

Such funds often have world-class infrastructure that can operate at scale and minimize costs for investors as a whole.

Depending on how the fund is structured, inflows usually lead the fund to buy more of the commodity and as a result, create a reflexive loop where investors can attempt to corner pockets of a particular commodity and setup attractive risk/reward propositions as in the case of uranium which has been a great beneficiary of the Russia/Ukraine conflict.

ETFs that hold physical commodities and not futures/financial paper products to provide exposure to the commodity can participate in long-term price appreciation without continuously rolling the futures and incurring transaction costs.

There is limited downside to owning physical ETFs but such products might have a higher cost structure due to operating storage facilities and operational expenditures which might be lower if the individual set up storage themselves for certain commodities.

Did You Know?

Canadian asset manager Sprott and its Physical Uranium Trust have accumulated as much as 55.6 million pounds of uranium which is as much as one year’s worth of global uranium production, draining the spot market and positioning itself to benefit from a switch to nuclear energy to reduce dependence on Russian energy supply.

3. Investing in Commodity Producer Stocks

While owning the physical commodity is the best way to get commodity exposure, investing in stocks of commodity-producing companies can be a great alternative as such equities benefit from price appreciation and can increase dividends to investors which aren’t present when holding physical commodities.

Commodity producers can take advantage of bull markets in the underlying asset as they are best positioned to generate higher revenues with more or less the same cost structure.

Further, such equities are a much larger asset class than other strategies which accommodate larger institutional investors.

The drawback to investing in commodity producers is that commodities move in boom and bust cycles.

Despite higher spot prices, commodity producers can be locked into long term price contracts or hedging programs capping the prices they’d receive for a certain period, minimizing their ability to participate meaningfully in price appreciation of the underlying commodity.

Also, an inflationary environment causes an uptick in the cost of production as all inputs get more expensive, thereby diminishing margins.

4. Commodity Futures

Commodity futures are instruments representing interests in energy, metals and agricultural products that are traded nearly 24×7 with a decent amount of liquidity.

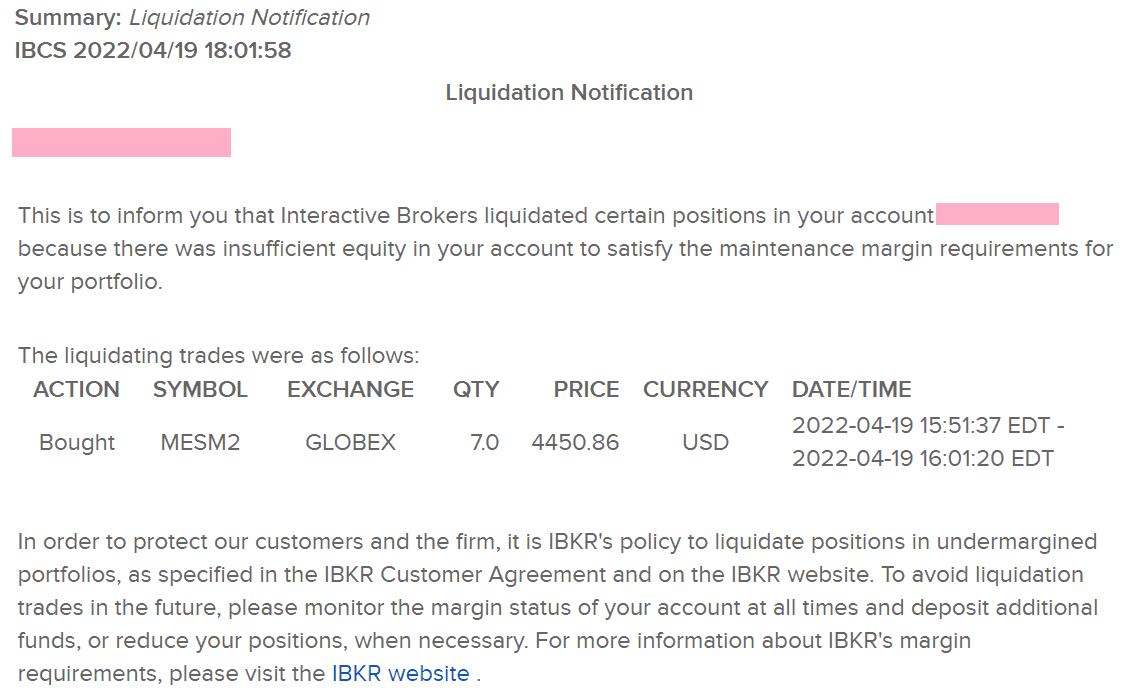

Margin accounts are necessary to trade futures and since these products employ leverage, it is important to size positions appropriately to avoid taking larger than necessary positions.

Positions are marked to market daily and it is necessary to meet maintenance margin requirements.

Otherwise, the broker will issue margin calls and liquidate positions until margin requirements are satisfied.

Commodity futures are an extremely liquid, direct way to participate in various commodity markets with leverage.

Such products can be settled financially or be taken into expiry to settle physically at the exchange’s specified delivery point.

Commodity futures are riskier products and need to be used by sophisticated investors as losses can exceed initial investments in volatile price moves.

Discretion, along with sound risk management processes are warranted.

During the early days of the pandemic, WTI front-month contracts that were expiring traded as low as negative -$38 as Cushing’s storage capacity (~90,000 barrels) was exhausted as global oil demand was decimated overnight due to lockdowns.

5. Commodity Trading Advisor (CTAs)

Commodity Trading Advisors gained popularity as commodity futures took off for hedging and speculative purposes as more and more markets were added with good liquidity behind those instruments.

CTAs have now evolved and trade more than commodities markets with some large CTAs having $50+ BN under management, trading virtually all tradeable future markets.

Their main draw is automated, system-based trading characteristics that use predetermined entry and exit points to eliminate emotional decision-making and take a more scientific approach to allocating capital.

Such funds have to register with the Commodities Futures Trading Commission (CFTC) and the National Futures Association and have to comply with their enforced regulations and make appropriate disclosures.

CTAs are professionally managed, rules-based investing methodologies that can participate in long-term price movements and capture large run ups in prices with holding periods as long as several years for some funds.

With the proliferation of several trend following algos, CTAs have found it difficult to trade long term trends without much larger stop losses as markets have become more choppy and there is a significant distortion in the noise/signal ratio making it hard to generate alpha.

While it is important to be aware of CTAs and their impact on the marketplace, individual investors may not be qualified to invest in these funds and might have to become qualified or accredited investors in order to invest.

Pros of Commodity Investing

Inflation Hedge

Commodities thrive in inflationary periods and act as effective hedges against rising prices.

Recent fiscal and monetary stimulus during the pandemic with severe supply-side constraints and limited investment in capacity for most commodity producers has teed off a commodity bull run.

By investing in commodities, investors can brace for an economic slowdown brought by demand-side destruction caused by high input prices.

Potential Returns

Commodities prices follow a boom and bust cycle lasting several years.

Investors that are positioned to take advantage and catch one of these cycles early on can benefit from such price moves and earn healthy profits during the run-up.

Uncorrelated Returns

Commodity prices move based on fundamental factors such as demand and supply, catalysts that accelerate demand or limit supply and other commodity-specific data.

However, commodities have their own sub-market metrics that can make them uncorrelated to the broader financial markets, making them relevant as an uncorrelated lever for effective portfolio construction.

Cons of Commodity Investing

Geopolitical Risks

Commodity producers domiciled abroad and owning assets in different markets can be adversely impacted by geopolitical risks.

While such crises often lead to a spike in prices in the short term, they have material impacts on the regulatory environment and can lead to sanctions or foreign exchange volatility.

Price Volatility

Commodity prices can be impacted in the short term by several factors and can present volatility for spot markets.

Such price movements can shake out investors using leverage or those that have large positions and tight stops.

Commodity investors need to be able to stomach heightened volatility and size positions appropriately while investing.

Commodity ETFs

ETFs that hold financial products to replicate returns of the underlying commodity will use futures contracts to get such exposure.

However, as these contracts get closer to expiry, they are rolled forward and investors pay the roll on such instruments.

Roll can be positive as well if the specific commodity is in backwardation but usually, such commodity ETFs find it hard to replicate the exact returns of the spot commodity and present some slippage in terms of tracking errors.

Are Commodities a Good Investment?

Commodities and equities of commodity producers can be great investments depending on the underlying macroeconomic setup and risk landscape.

But in general, investors should allocate a certain amount of their portfolio to commodities and vary that percentage depending on forward inflation expectations, stage of the business cycle and other relevant factors.

In the present economic environment, it can be said that we are in a cycle of rolling bubbles as each commodity has experienced bullish price action and portfolios without any commodity exposure have underperformed.