A bank draft is a financial instrument used to make large payments without the need to withdraw cash.

Bank drafts are guaranteed by financial institutions, meaning the individual or entity accepting payment has assurances that they will receive the funds.

A bank draft payment is the equivalent of a cash payment.

How a Bank Draft Works

Here’s an overview of how a bank draft works in practice:

1. The payer requests a bank draft for a specific amount at their bank.

The bank then reviews the payer’s account balance to verify that they have sufficient funds to cover the amount of the draft.

After the verification process is complete, the bank withdraws the funds from the payer’s account.

It issues the bank draft, which is a physical document that bears the intended recipient’s name.

2. The payer’s bank transfers the funds to their reserve account.

The funds remain in this account until the payee deposits the draft.

A bank’s reserve account contains bank deposits set aside to ensure withdrawal requests are honoured.

3. The payer delivers the draft to the payee.

This can be done personally or by mail.

4. The payee deposits the bank draft in their account.

Before accepting the draft, the bank confirms the payee’s identity and waits for the money to clear, which can take 3 – 5 business days.

Cancelling a Bank Draft

A unique aspect of a bank draft is that you’re unable to cancel it once it’s been issued.

The reason for this is once the funds have left the payer’s account and are sitting in the bank’s reserve account, the payment has already taken place.

When your financial institution presents to you a bank draft that you’ve requested, think of it as though you’ve already made your payment in cash to the payee.

A bank draft is synonymous with a cash payment – it’s erroneous to assume it functions like a cheque.

The only way you can “cancel” a bank draft is to have the payee deposit the draft and then return the money to you.

Are Bank Drafts Safe?

Yes. While a bank draft is equivalent to a large cash payment, it offers an additional layer of safety because the payer’s bank guarantees it.

As such, it’s also more secure than a cheque, which can bounce if the payer has insufficient funds in their account to cover it.

In addition, only the individual whose name is inscribed on the bank draft can deposit it.

This feature prevents unauthorized persons from cashing it.

Despite their safety, bank drafts have one shortcoming: they’re a physical document.

As a result, they’re prone to theft and damage.

Or they may go missing when in transit.

Should any of these scenarios occur, the payer is generally on the hook to replace the funds.

Suppose you obtain a bank draft to pay for a used vehicle, which you send by mail to the seller.

After some time, you discover the draft never arrived at its destination.

In this case, you should notify your financial institution right away and provide them with your draft reference number.

In the worst-case scenario, the bank will ask you to replenish your account with enough funds to cover the draft amount before issuing you a replacement draft.

However, suppose you’re able to persuade your bank not to pursue this route.

In that case, they may, instead, only ask you to sign a Lost Document Bond, personally guaranteeing that no one will cash the lost draft.

Ensure you review your financial institution’s policy regarding lost or stolen drafts.

To mitigate these risks, consider personally delivering a bank draft to the payee.

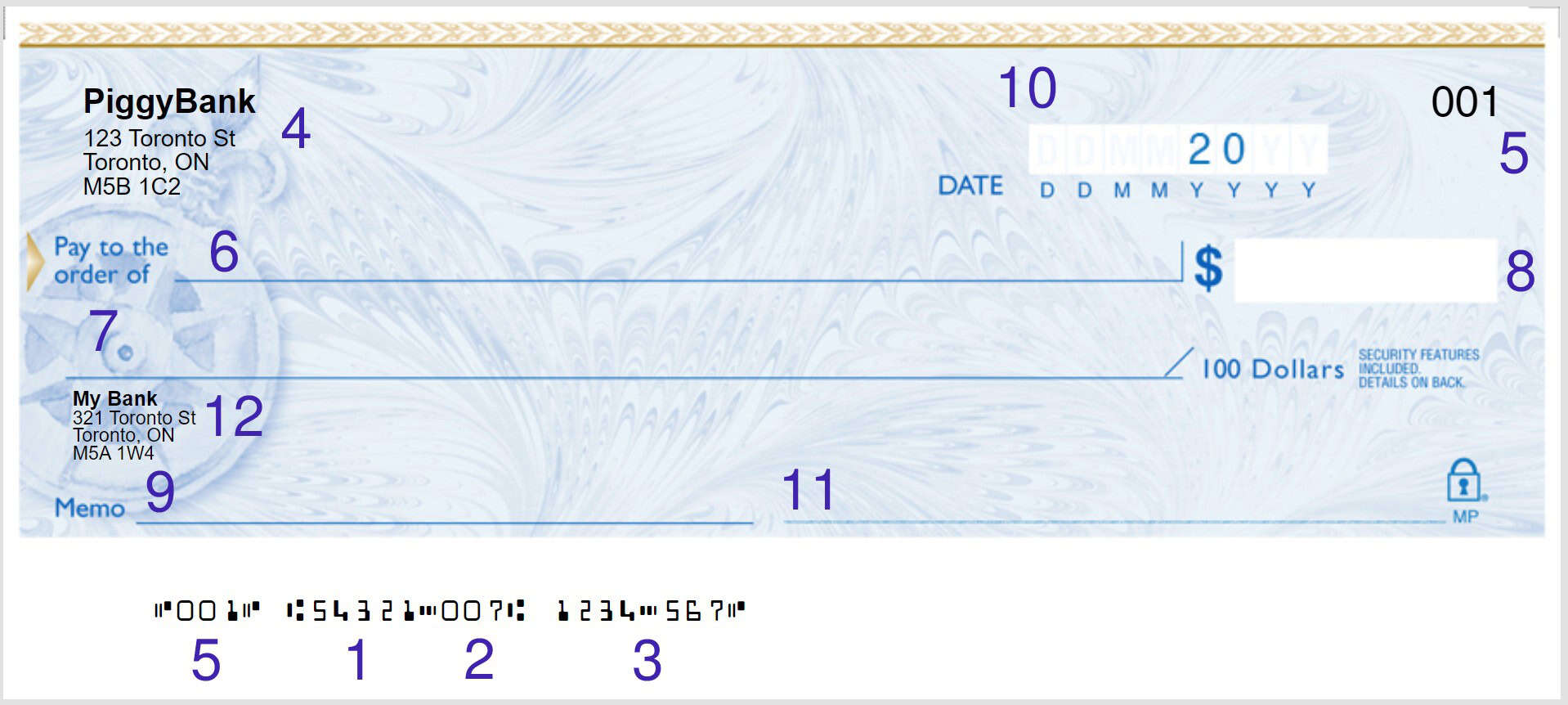

Bank Drafts vs Cheques

Here are the key differences between a bank draft and a cheque:

- A bank draft is issued by the payer’s bank, while the payer issues a cheque.

- Since the payer’s bank guarantees a bank draft, the payee is sure to receive the funds. When deposited by the payee, a cheque can bounce due to an insufficient balance in the payer’s account.

- A bank draft doesn’t have an expiry date – it can be cashed at any time by the payee. Conversely, a cheque becomes stale-dated after six months, at which point financial institutions may decide not to accept it.

- A bank draft can’t be cancelled once issued, as it represents a transaction that has already taken place. With a cheque, the payer can place a stop payment to void it while it’s in transit.

- A bank draft doesn’t contain the signature of the payer, while a cheque does.