Your Canada Pension Plan (CPP) or Quebec Pension Plan (QPP) — for those who reside in Quebec – is considered to be income and thus is subject to tax by the Canada Revenue Agency (CRA).

When you are at least 60 years of age and you decide to retire, you may be eligible to receive CPP payments.

To receive CPP payments, you will need to apply and the amount you receive will depend on your average earnings when you were employed or self-employed, the age you retire, and how much you contributed to the Canada Pension Plan.

Are taxes already deducted from my CPP payment?

Canada Pension Plan payments you receive are not automatically taxed.

This means that taxes are not withheld on the income you receive like they usually would be when you’re employed.

You will need to report this income in your tax return for the year that you receive the payment, and you may have to pay income taxes on the CPP amounts you receive.

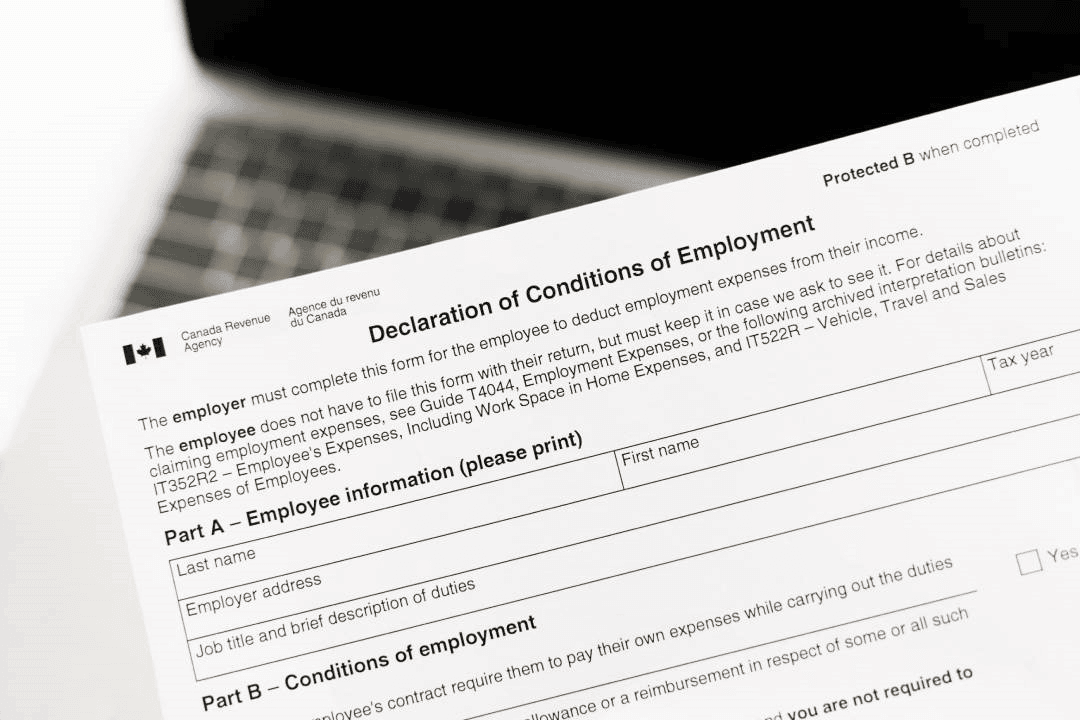

Alternatively, you can request that monthly federal income tax deductions be taken from your monthly CPP payments.

You can send this request through your My Service Canada Account or simply complete and submit the following form.

If you decide to submit the request by paper, you can mail it to a Service Canada office or drop it off in person.

When you voluntarily request to have tax withheld on your monthly Canada Pension Plan payments, you can indicate to set the tax deduction as an amount or as a percentage of your payments.

You can request to modify your voluntary tax deduction at a future date using the same form.

Factors to Consider Alongside CPP Payments

While your Canada Pension Payments are subject to tax, you will generally fall within a lower tax bracket when you retire, causing your income tax to be relatively low.

However, if you receive income from other sources such as a Registered Retirement Savings Plan, rental income, or other investment income, this may impact your income tax bracket.

Some sources of retirement income to consider when it comes to managing your overall income tax:

- Registered Retirement Savings Plan (RRSP) Withdrawals: Before retirement, when you make RRSP contributions, you get income tax deductions and therefore pay lower taxes on your income. In addition to this tax benefit, your contributions in your RRSP can grow tax-free provided they remain in the account. However, when you withdraw money from your RRSP in retirement, you will need to pay tax on the withdrawals, as they are considered to be income. RRSP withdrawals will increase your overall income and can possibly bump you into a higher income tax bracket.

- Old Age Security Payments: If you qualify to receive Old Age Security (OAS) pension payments in retirement, these payments will be considered income as well, and thus taxed accordingly. As with any other retirement income you receive, OAS income can increase your tax bracket and can lead to higher taxes in retirement. You can also elect to have tax deductions automatically withheld from your Old Age Security payments.

- Other Retirement Income: Any other type of income received in retirement can increase your tax bracket. This may include income from a business, benefits, rental property, investments, a Registered Retirement Income Fund (RRIF), life income fund (LIF), other annuities, etc. However, income received from your tax-free savings account (TFSA) will not be taxed.